.jpg)

What’s the best way to make a budget? There’s no right or wrong answer. Over time, many people learn what works (and doesn’t work) for them when creating a budget. But if you’re learning to budget for the first time, it can help to have a clear method to follow.

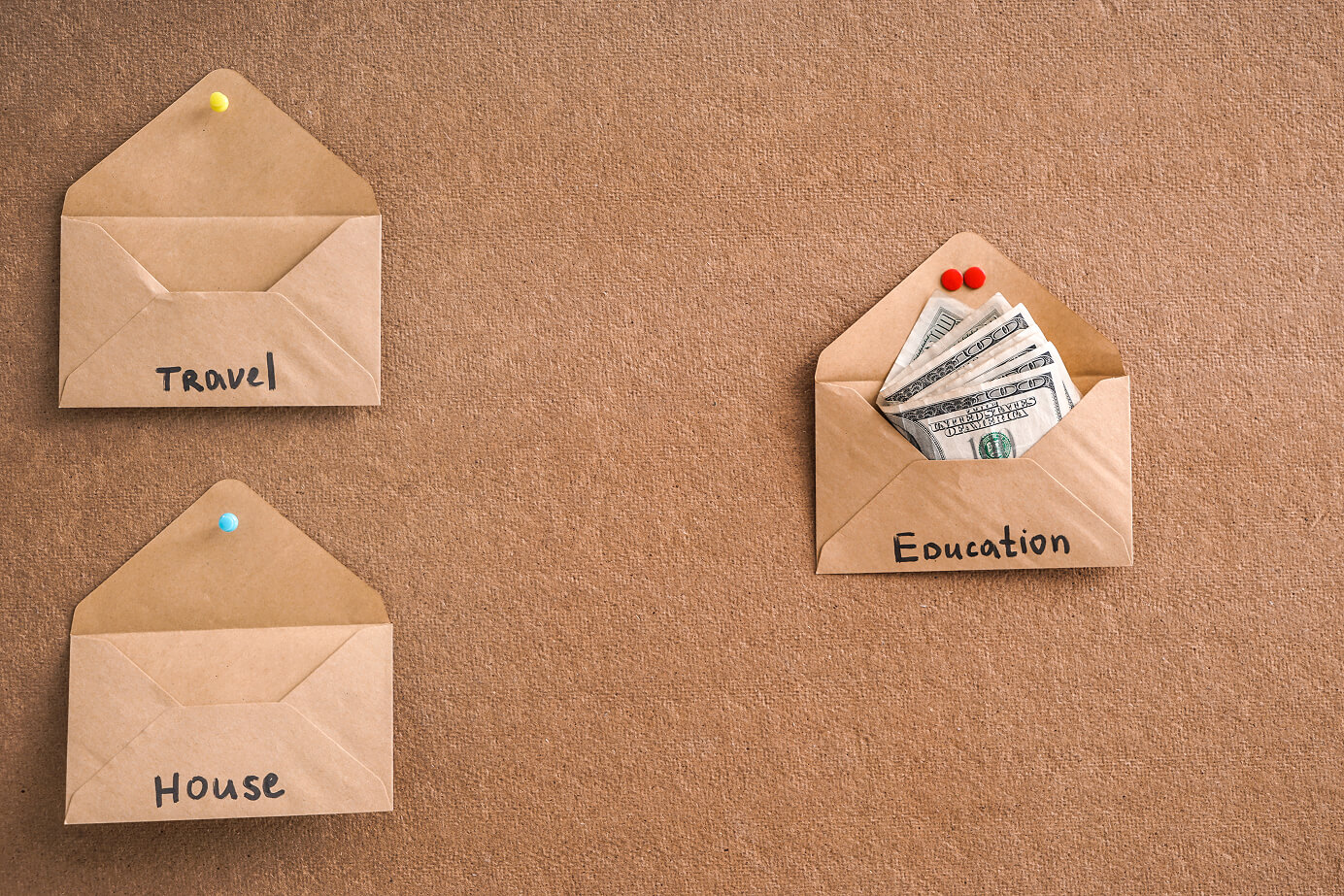

That’s where the envelope budgeting method comes in. This tried-and-true strategy can help people of all backgrounds keep track of their money. And depending on your preferences, you can build it around actual, physical envelopes or go digital.

What is the envelope budgeting method?

The envelope budgeting method is intended to make spending feel more tangible. To implement it, simply divide your spending into categories and assign an envelope to each category. Over the course of the month, you’ll limit yourself to the money in each envelope.

Traditionally, the envelope budgeting method is done the old-fashioned way: with cash and paper envelopes. However, if you’d rather keep things digital, you can create a spreadsheet or use an app to create “envelopes” and track your spending.

How does the envelope budgeting method work?

Thinking about trying the envelope budgeting method? Here’s a step-by-step guide to get you started.

Step 1: List your monthly income

Before you start creating spending categories, write down your monthly income. You’ll need an idea of how much you’ll make in the month ahead. If your income varies from month to month, it’s okay to estimate.

Step 2: Identify your spending categories

Most people have numerous expenses each month. Those can generally be divided into two broad categories:

- Fixed: Expenses that stay the same from month to month (like rent)

- Variable: Expenses that can fluctuate (like groceries)

First, write down your fixed expenses. Add them up and subtract them from your total income. Then, divide what’s left between your variable spending categories.

Before you start assigning cash amounts to each of your envelopes, however, you’ll need to identify your other spending categories. Some people like to have a handful of broad categories, while others would rather make several narrower categories. How you go about it is entirely up to you.

Here are some examples of variable expenses you may want to include:

- Groceries

- Dining out

- Gas

- Entertainment

- Utilities

- Pet care

Many budgeters opt to create a “miscellaneous” category in case they encounter an expense that doesn’t fit neatly into any single other category.

Step 3: Assign a cash amount to each envelope

This step represents the heart of this budgeting strategy. Label each envelope with a category and assign it a cash amount. If you want, you can start with your fixed expenses because their cash amounts have been decided for you. For instance, you might label one envelope “Rent: $800” and then stuff it with your rent money.

Assigning cash values to variable expenses can be a little more complicated. If you’ve never created a budget before, it may help to look at recent bank statements to get an idea of where your money goes each month.

Here’s an example list of possible envelopes:

- Rent: $800

- Groceries: $200

- Dining Out: $50

- Gas: $70

- Entertainment: $80

- Utilities: $100

- Pet Care: $100

- Miscellaneous: $100

Remember that the point of envelope budgeting is to limit yourself to the cash in each envelope. When in doubt, it’s a good idea to budget more than you think you’ll need. If you have money left over, you can save it or put it toward debt repayment.

Once you’ve assigned a cash value to each category (and double-checked that you haven’t allotted more than your total income), it’s time to put cash in each envelope.

Keep your envelopes in a safe place, ideally a locked safe that only you can access.

Step 4: Spend only what is in each envelope

Now comes the challenge: Over the course of the month, you can only spend what’s in each envelope. To really get a sense of how you’re spending, write each transaction on the relevant envelope. For example, if you have to take your pet to the vet, you might write “Vet Bill: $80” on your pet-care envelope.

Remember, if you run out of money in one envelope, you must stop spending in that category until next month.

Step 5: Adjust your envelopes each month

Learning to budget is an ongoing process. If this is your first time trying the envelope method, you might find that you need to make some adjustments for the next month.

For example, if you only spent $20 on entertainment and your entertainment envelope had $100, you might lower your entertainment budget for the next four weeks and increase the budget for another category.

Pros and cons of envelope budgeting

The envelope budgeting method is one of the more popular budgets out there, but that doesn’t necessarily mean that it’s the best fit for you. Before you go buy a stack of envelopes and take cash out of your bank account, it’s wise to consider the benefits and drawbacks of this system.

Here are some of the advantages of envelope budgeting:

- It helps prevent overspending

- It’s simple and easy to follow

- It forces you to prioritize

- It’s a great way to build discipline

- Holding cash in your hands may help you make more thoughtful spending decisions

However, there are also some potential downsides, including:

- Taking cash out of your bank account all at once can be inconvenient

- It may be impractical if you shop or pay bills online

- Filling envelopes at the start of the month can be a challenge if you’re paid weekly or biweekly

- There’s a risk that you could lose an envelope

Some critics of this method have pointed out that your money can earn more interest if you keep it in a savings account rather than in cash. If you like the idea of the envelope method but find physical envelopes impractical, you can always create envelopes digitally.

The right budget makes all the difference

There’s no shortage of budgeting strategies out there, and the envelope method may not be right for everyone. However, because it helps users track each dollar and makes them prioritize their spending, it’s a great introduction for those who haven’t seriously budgeted before.

If you’re ready to start tracking and managing your spending, Grant Cash Advance is here for you. We connect eligible users with cash advances from $25 to $500, but that’s not all we do. We also offer budgeting tools and personalized financial insights to help you get closer to your goals.

Getting started is free, and there’s no credit check. Download Grant Cash Advance and see if you qualify for an advance today.

Frequently Asked Questions

About the author

Sarah Edwards is passionate about financial literacy and helping readers navigate their money with confidence. She specializes in breaking down complex financial topics into clear, accessible language and regularly covers personal finance, credit, debt, insurance, crypto, and small business. Sarah has contributed to publications such as NerdWallet, MoneyLion, Benzinga, and others.